AWP Alliance News Global service

Innovative financial news service that combines high-quality journalism with AI-support speed and breadth of coverage.

AWP Alliance News Global offers the most comprehensive market coverage, with 20,000 or more companies covered with brief summaries of disclosure. Some 2,000 of the most traded and influential of these companies receive editorial reporting on a regular basis.

The comprehensive equity news reporting is complemented with economic and political news from 50 countries, including economic indicators from the lock-up, central bank decision, regulation and more. Our stock market reports also track currencies, bonds and commodities, and each of these markets also have their own dedicated market reports throughout the day.

AWP Alliance News Global is the product of a partnership of experienced international news agencies.

- 7,000+ companies in North America

- ‘Speedflash’ engine for earnings

- 7,000+ companies in Europe

- editorially guided AI news briefs

- 6,000+ companies in Asia-Pacific

- company and economic calendars

- economic news from 50 countries

- economic indicator actuals data feed

- central bank decisions

- multi-media top news and pictures

- forex, bonds, oil and gold markets

- retail Investor and regional packages also available

Key Features

Flash Headlines

Flash Headlines

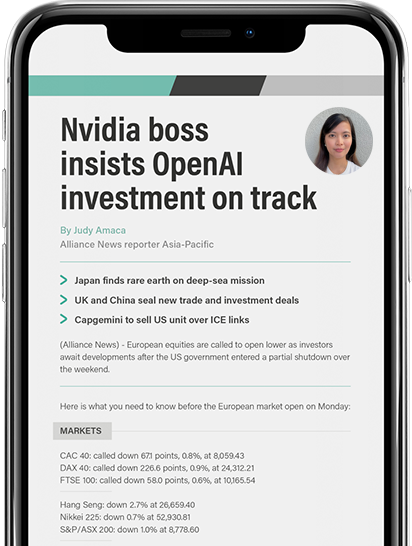

*Nvidia call: expects OpenAI investment to translate to extraordinary returns

Wed 19 Nov 2025 22:50 GMT

*Nvidia call: on track to hit USD500b Datacentre revenue forecast by 2026

Wed 19 Nov 2025 22:34 GMT

*Nvidia call: AI is transforming existing applications while enabling entirely new ones

Wed 19 Nov 2025 22:28 GMT

*Nvidia call: accelerated computing has reached a tipping point

Wed 19 Nov 2025 22:28 GMT

*Nvidia call: working to hold gross margins in mid-70s in FY27 despite higher input costs

Wed 19 Nov 2025 22:26 GMT

*Nvidia call: not assuming any data centre compute revenue from China in Q4

Wed 19 Nov 2025 22:25 GMT

*Nvidia call: GB300 contributed around two-thirds of total Blackwell revenue

Wed 19 Nov 2025 22:18 GMT

*Nvidia call: ecosystem will be ready for a fast Rubin ramp

Wed 19 Nov 2025 22:15 GMT

*Nvidia call: Rubin platform on-track to ramp-in the second-half of 2026

Wed 19 Nov 2025 22:14 GMT

*Nvidia call: sizeable H20 sales orders failed to materialise due to geopolitical issues

Wed 19 Nov 2025 22:13 GMT

*Nvidia call: clouds are sold-out, GPU installed-base fully utilised

Wed 19 Nov 2025 22:10 GMT

*Nvidia call: demand for AI infrastructure continues to exceed our expectations

Wed 19 Nov 2025 22:09 GMT

*Nvidia call: estimates USD3-4t in annual AI infrastructure build by 2030

Wed 19 Nov 2025 22:08 GMT

*Nvidia call: have visibility to USD500b in Blackwell and Rubin revenue from 2025 to 2026

Wed 19 Nov 2025 22:07 GMT

*Nvidia Declares Quarterly Dividend of USD 0.01, Record Date 12/4/2025

Wed 19 Nov 2025 21:41 GMT

*Nvidia forecasts Q4 revenue of USD65b, plus or minus 2%

Wed 19 Nov 2025 21:27 GMT

*Nvidia Q3 EPS USD1.30 vs. USD0.78 Year Ago

Wed 19 Nov 2025 21:24 GMT

*Nvidia Q3 revenue USD57.01b vs USD35.08b YoY

Wed 19 Nov 2025 21:20 GMT

*Nvidia Q3 diluted EPS USD1.3 vs USD0.78 YoY

Wed 19 Nov 2025 21:20 GMT

*Nvidia Q3 net income USD31.91b vs USD19.31b YoY

Wed 19 Nov 2025 21:20 GMT

*GET READY: Nvidia Q3 results; USD55.10b revenue, USD1.25 EPS forecast – VA consensus

Wed 19 Nov 2025 20:57 GMT

AI Briefs

AI Briefs

30 Jan 2026, 15:12:42 GMT

AB InBev Reacquires 49.9% Stake in US Metal Container Plants for USD 2.9 Billion

(AWP Alliance News) – Anheuser-Busch InBev SA (AB InBev) has completed the reacquisition of a 49.9% minority stake in its US-based metal container plants from a consortium of institutional investors led and/or advised by affiliates of Apollo Global Management, Inc. The transaction was valued at approximately 2.9 billion USD. AB InBev had previously announced its intention to exercise its right to reacquire this minority stake on January 6th.

https://docs.publicnow.com/56B96FD82E081C2B7864A78B811FCFF02992B654

Disclaimer: This news brief was created using generative artificial intelligence. AB – Anheuser-Busch InBev SA published the original content used to generate this news brief on January 30, 2026, and is solely responsible for the information contained therein.

Global Briefing

Global Briefing

Extra

Extra

15 Jan 2026 17:26 GMT

EXTRA: Goldman looks for M&A to kick off flywheel of activity in 2026

(Alliance News) – Goldman Sachs Group Inc on Thursday said it expects investment banking to have a “multiplier” impact on the rest of its business in 2026, driving another year of growth.

The Wall Street investment bank pleased investors with better-than-expected revenue and earnings, although costs were stronger than forecast.

Shares fluctuated in New York on Thursday, but were trading 4.2% higher at USD971.85 in the early afternoon.

“GS shares have been near unstoppable into this print, and so despite the strong revenue print we think the shares trade in-line,” commented UBS analyst Erika Najarian.

The Wall Street investment bank reported net earnings of USD4.62 billion in the three months to December, up 12% from USD4.11 billion the year prior.

Basic earnings per share increased 17% to USD14.21 from USD12.13 the year prior, and ahead of Visible Alpha consensus of USD11.40.

Reported revenue slipped 2.4% to USD13.54 billion from USD13.87 billion. Within this, net interest income jumped 58% to USD3.71 billion from USD2.35 billion.

Goldman Sachs said lower revenue reflected negative net revenue in Platform Solutions due to a reduction in net sales of USD2.26 billion from markdowns on the outstanding credit card portfolio related to the transfer of the Apple Card loans following the agreement with JPMorgan Chase & Co and Apple Inc.

Stripping this out, revenue reached USD15.80 billion, ahead of Visible Alpha consensus of USD14.26 billion.

Goldman said the fall in Platform Solutions was “largely offset by significantly” higher net revenues in Global Banking & Markets.

JPMorgan analyst Kian Abouhossein said the strong results should prompt mid-single digit consensus EPS upgrades in 2026.

Net revenue in Global Banking & Markets was USD10.41 billion in the fourth quarter, 22% higher than last year, and 2% higher sequentially.

Investment banking fees jumped 25% year-on-year, primarily due to significantly higher net revenues in Advisory.

Net revenue in debt underwriting was higher, reflecting significantly higher net revenue from asset-backed activity, while revenue in equity underwriting was slightly higher.

Goldman’s investment banking fees backlog increased compared with the end of the third quarter.

Revenue in Asset & Wealth Management was flat year-on-year, with significantly lower revenue in investments largely offset by higher management and other fees.

Najarian at UBS noted Investment Banking was 3% ahead of consensus, Advisory was strong, Markets “notable” at an 11% beat and Equities was a “shining star”, beating the Street by 17%.

Chief Financial Officer Denis Coleman said in 2025 Goldman maintained its number-one position in the league tables for announced and completed M&A and also ranked first-in leverage lending.

Further, Goldman ranked third in equity underwriting and second in common stock offerings, convertibles and high-yield offerings.

The strong performance in investment banking is set to continue into 2026, Goldman believes.

Chief Executive David Solomon expects investment banking activity to accelerate in 2026 noting deal backlog is at its highest-level in four years.

In 2025, alone, Goldman advised on more than USD1.6 trillion of announced M&A transaction volumes over USD250 billion ahead of the next closest peer, the CEO said.

“M&A transactions often kick-off a flywheel of activity across our entire franchise, whether it’s acquisition financing, hedging activity, secondary market making or investing opportunities for [Asset Wealth Management] clients, it is unquestionable that there is a significant multiplier effect,” he explained.

Solomon said he is optimistic about the outlook for equity and debt underwriting, particularly amid the resurgence in the initial public offer market and a higher acquisition finance-related activity.

“Barring some sort of an exogenous event that slows it down, we’re going to have a pretty constructive environment for those activities,” the CEO said.

“CEOs definitely believe that the art of the deal and scaled consolidation is possible now. And when CEOs see that opportunity, because scale matters so much in business, business is so competitive, CEOs get very front-footed.” Solomon stated.

Solomon said Goldman sees even more opportunities to further strengthen its franchise, it’s working to close share gaps with key client segments and geographically is looking to close the share gap in Asia.

The bank raised its mid-term Asset and Wealth Management pretax margin target to 30% from mid-20s and is targeting returns now of high teens compared to mid teens before.

“We’re comfortable putting that target out and that, of course, elevates the overall performance of the firm,” Solomon added.

With regard to M&A, the Goldman boss stressed the bar for “transformational M&A remains very-high.”

It has to be high, because there are “very few really, really great large businesses”, and “most of them are not for-sale and available”.

But the bank sees meaningful opportunities to deploy capital across the franchise, including “leaning into” acquisition financing as M&A activity accelerates, supporting growth in equities and fix financing and increasing lending to ultra-high net-worth clients.

Goldman also has capacity to return more capital to shareholders.

The bank increased its quarterly dividend to USD4.50 from USD4.00 a year ago.

Goldman said it will remain “dynamic” in executing share repurchases, although its “unwavering” focus remains on maintaining a disciplined risk management framework and robust standards.

Commenting on the mid-teens return on equity target, Solomon said the “this is an environment where the potential to be positioned to exceed targets in the near-term is there.”

In the fourth quarter, return on equity totalled 16%.

He pointed out the regulatory environment in the last five years put “costs and burdens on the firm that we now won’t have going-forward that actually gives us flexibility to invest over-time in other things that drive growth.”

On AI, Solomon said the technology offers an opportunity to drive productivity, which will add to capacity to invest in business.

“It’s not just to take cost-out, but it’s also to free-up capacity to invest in other areas where we see growth opportunities that we’ve been a little bit constrained,” he explained.

Goldman said provision for credit losses was a net benefit of USD2.12 billion for the fourth quarter compared with net provisions of USD351 million a year ago, reflecting a net release related to the Apple Card portfolio.

Operating expenses increased 18% year-on-year in the quarter, reflecting “significantly” higher compensation and benefits expenses and higher transaction based expenses.

By Jeremy Cutler, Alliance News reporter

Comments and questions to newsroom@alliancenews.com

Copyright 2026 Alliance News Ltd. All Rights Reserved.

Broker Ratings

Broker Ratings

16 Jan 2026 12:32 GMT

GLOBAL BROKER RATINGS: UBS cuts Sanofi; Citi raises Intel

(Alliance News) – The following global blue-chips received analyst recommendations Friday and Thursday:

———-

BASIC RESOURCES

———-

Deutsche Bank Research raises Aurubis price target to 140 (112) EUR – ‘hold’

———-

UBS raises Wacker Chemie price target to 84 (79) EUR – ‘buy’

———-

Barclays cuts Brenntag price target to 42 (46) EUR – ‘equal weight’

———-

Barclays cuts BASF price target to 40 (41) EUR – ‘equal weight’

———-

Barclays cuts Lanxess price target to 14 (15) EUR – ‘underweight’

———-

RBC raises Glencore price target to 530 (480) pence – ‘outperform’

———-

CONSUMER DISCRETIONARY

———-

Metzler cuts Sixt price target to 90 (101) EUR – ‘buy’

———-

Jefferies cuts Dunelm price target to 1,075 (1,131) pence – ‘hold’

———-

CONSUMER STAPLES

———-

Berenberg raises Unilever price target to 5,600 (5,530) pence – ‘buy’

———-

Barclays raises Ocado price target to 175 (160) pence – ‘underweight’

———-

Morgan Stanley cuts Kraft Heinz to ‘underweight’ (equal-weight) – price target 24 (27) USD

———-

FINANCIALS

———-

Jefferies cuts Deutsche Boerse price target to 240 (245) EUR – ‘hold’

———-

Goldman Sachs raises ING price target to 26 (25.80) EUR – ‘buy’

———-

Oddo BHF cuts Aroundtown to ‘underperform’ (neutral) – price target 2.60 (3.10) EUR

———-

Barclays cuts Munich Re price target to 616 (625) EUR – ‘overweight’

———-

Kepler Cheuvreux starts Munich Re with ‘buy’ – price target 600 EUR

———-

KBW cuts Swiss Re to ‘underperform’ (market perform) – price target 120 (140) CHF

———-

Deutsche Bank Research raises Rathbones price target to 2,100 (2,000) pence – ‘hold’

———-

Citigroup raises St James’s Place price target to 1,790 (1,590) pence – ‘buy’

———-

UBS cuts Wise price target to 1,240 (1,320) pence – ‘buy’

———-

RBC raises Close Brothers to ‘outperform’ – price target 625 (475) pence

———-

Deutsche Bank Research raises Ashmore target to 140 (100) pence – ‘sell’

———-

Jefferies raises Goldman Sachs price target to 1,125 (1,087) USD – ‘buy’

———-

JPMorgan raises Goldman Sachs price target to 815 (775) USD – ‘neutral’

———-

Jefferies raises Morgan Stanley price target to 221 (212) USD – ‘buy’

———-

JPMorgan raises Morgan Stanley price target to 173 (162) USD – ‘neutral’

———-

LBBW raises JPMorgan price target to 247 (244) USD – ‘sell’

———-

HEALTH CARE

———-

Deutsche Bank Research cuts Sanofi price target to 105 (110) EUR – ‘buy’

———-

UBS cuts Sanofi to ‘neutral’ (buy)

———-

Barclays cuts Redcare Pharmacy price target to 110 (130) EUR – ‘overweight’

———-

UBS raises Roche price target to 384 (356) CHF – ‘buy’

———-

Goldman Sachs raises Roche to ‘neutral’ – price target 365 CHF

———-

Deutsche Bank Research raises Novartis price target to 125 (120) CHF – ‘buy’

———-

UBS raises Novartis price target to 116 (102) CHF – ‘neutral’

———-

UBS raises AstraZeneca price target to 16,300 (14,200) pence – ‘buy’

———-

Deutsche Bank Research raises AstraZeneca price target to 11,000 (10,500) pence – ‘sell’

———-

Berenberg raises Genus price target to 3,250 (3,050) pence – ‘buy’

———-

UBS raises GSK price target to 1,940 (1,900) pence – ‘neutral’

———-

Deutsche Bank Research raises GSK price target to 1,675 (1,600) pence – ‘hold’

———-

INDUSTRIALS

———-

Deutsche Bank Research raises Oxford Instruments price target to 2,675 (2,435) pence – ‘buy’

———-

Berenberg raises Oxford Instruments price target to 2,700 (2,400) pence – ‘buy’

———-

RBC cuts Grafton price target to 1,170 (1,190) pence – ‘outperform’

———-

RBC cuts Travis Perkins price target to 850 (865) pence – ‘outperform’

———-

Deutsche Bank Research cuts Essentra price target to 150 (165) pence – ‘buy’

———-

JPMorgan raises Honeywell to ‘overweight’ (neutral) – price target 255 (218) USD

———-

JPMorgan cuts 3M to ‘neutral’ (overweight) – price target 182 USD

———-

ENERGY

———-

Berenberg cuts BP price target to 520 (525) pence – ‘buy’

———-

TECHNOLOGY

———-

Morgan Stanley raises ASML price target to 1,400 (1,000) EUR – ‘overweight’

———-

Bank of America raises ASML price target to 1,363 (1,205) EUR – ‘buy’

———-

Deutsche Bank Research cuts ATOSS Software price target to 135 (140) EUR – ‘buy’

———-

Barclays cuts Ionos price target to 39 (42) EUR – ‘overweight’

———-

Barclays cuts freenet price target to 32 (34) EUR – ‘equal weight’

———-

Barclays cuts Delivery Hero price target to 36.40 (38.10) EUR – ‘overweight’

———-

Citigroup raises Intel to ‘neutral’ (sell) – price target 50 (29) USD

———-

TELECOMMUNICATIONS

———-

Jefferies cuts Inwit price target to 8 (10,10) EUR – ‘hold’

———-

Barclays cuts Gamma Communications price target to 1,600 (1,700) pence – ‘overweight’

———-

UTILITIES

———-

Metzler raises RWE price target to 59 (57) EUR – ‘buy’

———-

By Holly Munks, Alliance News reporter

Comments and questions to newsroom@alliancenews.com

Copyright 2026 Alliance News Ltd. All Rights Reserved.

Broker Notes

Broker Notes

14 Jan 2026 10:25 GMT

BROKER NOTES: “Doing right thing” won’t be easy for Bytes – Jefferies

Bytes Technology Group PLC – Surrey, England-based enterprise software – Jefferies lowers to ‘hold’ (buy) – price target 400 (447) pence.

The broker believes Bytes Technology’s management is approaching a period of “profit disruption” in the correct manner. However, “doing the right thing isn’t always easy”, Jefferies adds. “We think go-to-market changes could take longer than expected to bed down, while continued investment is likely to pressure 2027 earnings before interest and tax,” Jefferies predicts.

Bytes recently “realigned” its corporate sales team, the company noted back in October. “This will improve our customer proposition by enhancing account management, vendor relationships and solution/service delivery but resulted in an adjustment period as account managers adapted to the changes,” the firm had said. Jefferies says the shift is “disruptive” but should create efficiencies in the long-term. “However, change takes time and there is little help from flat end markets to grease the wheels. As a result, we see little upside to near term gross profits, while operating expenditure is likely to remain elevated,” Jefferies adds.

Current stock price in London: 354.00 pence, down 3.7% on Wednesday

12-month change: down 13%

Current stock price in Johannesburg: ZAR77.82, down 5.1% on Wednesday

12-month change: down 19%

By Eric Cunha, Alliance News news editor

Comments and questions to newsroom@alliancenews.com

Copyright 2026 Alliance News Ltd. All Rights Reserved.

In The Know

In The Know

09 Jan 2026 15:04 GMT

IN THE KNOW: L’Oreal boosted by UBS upgrade and positive JPM comments

(Alliance News) – Shares in L’Oreal SA jumped on Friday amid a rating upgrade from UBS and positive commentary from JPMorgan.

The Clichy, France-based personal care corporation stood 5.9% higher at EUR384.35 in Paris mid-Friday afternoon.

UBS upgraded L’Oreal to ‘buy’ from ‘neutral’ and raised its 12-month share price target to EUR430 from EUR367.

The Swiss bank said that for the first time in more than two years it sees L’Oreal’s investment case benefitting from a “rare combination of favourable factors”.

These are rapidly improving operational momentum owing to accelerating industry growth and enhanced market share momentum; upside to consensus; compelling valuation; and improved risk profile given the decreasing reliance on the fragrance category and company’s decision to not increase further its stake in Galderma.

UBS expects beauty market growth of 3.5% in 2025 as a whole, below its historical average of 4.3%.

However, this “unusually muted development” was mostly attributable to a slow start to the year, before growth started to pick up and, UBS estimates it reached 4% in the fourth quarter led by L’Oreal’s two largest markets of the US and China.

Looking ahead, UBS expects L’Oreal to continue to deliver superior growth compared to the industry, driven by structurally higher gross margins, long term mindset favouring reinvestments over significant operating margin expansion and continued stream of bolt-on deals.

Meanwhile, JPMorgan which has a ‘neutral’ rating on L’Oreal placed the company on ‘positive catalyst watch’ ahead of fourth quarter results.

“Following on from optimistic comments on US improvement and progressive China recovery at their capital markets day in December, subsequent data across US, Europe and China should reassure on underlying organic sales growth accelerating – which we expect at 5.9% in Q4 [versus] vs Q3 underlying at 4.9%,” JPM said.

On a reported basis, JPM expects fourth quarter like-for-like growth of 7.0% ahead of consensus at around 6%.

“We expect a short-term growth beat to be welcome, though a sustained re-rating in the shares will require a significant step up in growth outperformance, which we do not envision in FY26,” the broker added.

As a result, JPM placed the stock on ‘positive catalyst watch’ into full year results on February 12, where “we expect a strong end to 2025 combined with likely cautiously optimistic commentary for progressively improving beauty markets and L’Oreal’s own ‘Beauty Stimulus’ efforts to support the shares.”

By Jeremy Cutler, Alliance News reporter

Comments and questions to newsroom@alliancenews.com

Copyright 2026 Alliance News Ltd. All Rights Reserved.

Executive Interviews

Executive Interviews

20 Nov 2025 12:15 GMT

EXTRA: PayPoint pushes back earnings target but proves “resilient”

(Alliance News) – PayPoint PLC on Thursday reported lower half-year profit and said it is likely to take longer to achieve a key annual earnings target, but it expects to have largely overcome challenges by the second half of the year.

Shares in PayPoint were down 17% to 537.00 pence midday Thursday in London. The wider FTSE 250 index was up 0.1%. In the past 12 months, PayPoint’s stock has fallen 41%.

The Hertfordshire, England-based payments processor and retailing technology provider said pretax profit fell 14% to GBP19.9 million for the six months ended September 30 from GBP23.1 million, hurt mainly by increases to the cost of sales.

Underlying earnings before interest, tax, depreciation and amortisation slipped 0.5% to GBP37.3 million from GBP37.5 million. PayPoint had a “key” target to achieve an underlying Ebitda of GBP100 million for financial 2026, but said “it is likely we will take longer to do so”.

In an interview with Alliance News, Chief Executive Nick Wiles said the company is “probably going to achieve that target next year”, meaning financial 2027.

Wiles added that the company “broadly remained on track”, despite headwinds resulting from InPost’s Yodel acquisition, PayPoint’s acquisition of OBconnect Ltd, and revenue recognition timing changes.

The interim profit figure includes GBP5.8 million in adjusted items, comprising of GBP1.7 million in OBconnect costs and GBP3.2 million in legal fees incurred, as well as expenses associated with the company’s organisational framework.

OBconnect is an open-banking provider. Having contributed GBP1.9 million in the first half, Obconnect’s growth and monetising of opportunities were nonetheless slower than anticipated, PayPoint said.

“This first half has been more of a consolidation,” said CEO Wiles. “There’s enough visibility there to say that the Obconnect business will do better in the second half of this year compared to the second half of last year. That bump in the first half is largely going to get managed through to the second.”

PayPoint’s total revenue rose 6.7% to GBP144.1 million from GBP135.0 million. The company noted a 9.6% drop in revenue for its Love2shop segment, which fell to GBP17.0 million from GBP18.8 million. This was attributed to changes to the timing of revenue recognition for card expiry.

“What we have moved the accounting treatment to is an actual,” Wiles explained. “We actually only recognise revenue at the end of the life of a card.”

“The impact would be that the full value of…that card and its revenue will be recognised at the end of its life,” Wiles added. He said this more conservative approach makes management feel the “most comfortable” about the quality of their earnings.

Following InPost’s acquisition of Yodel, PayPoint said the combined business’ three-year commercial contract had “less favourable” terms for the company. The company noted it had “underappreciated the disruptive impact of the InPost/Yodel harmonisation”.

“The fallout of that puts some real pressure on our own parcels network in terms of our own volumes, our own service delivery,” said Wiles. “I think coming into the peak largely those operational challenges have been worked through the system.”

PayPoint declared an interim dividend of 19.8p per share, up 2.1% from 19.4p in the prior year. It added that it is “on course to generate returns to shareholders of over GBP90 million”.

For the next three years to the end of financial 2028, PayPoint said it aims to achieve net revenue growth in the range of 5% to 8% per year, establish an organisational framework and deliver a reduction of at least 20% of its issued share capital.

Wiles noted an “encouraging” rate of adoption from its launch of PayPoint BankLocal with Lloyds Banking Group PLC.

Asked about the likely impact of the UK government budget next week, Wiles said: “I don’t know whether there will be enough clarity from the budget next week for those uncertainties and for consumer confidence to be reinvigorated. It looks unlikely to me, and I would have thought the run up to Christmas is going to be more challenging for retailers in general, and that will make life more challenging for us as well.”

Regarding the half-year results, Wiles added: “I think overall a really resilient financial performance.”

By Roya Shahidi, Alliance News reporter

Comments and questions to newsroom@alliancenews.com

Copyright 2025 Alliance News Ltd. All Rights Reserved.

Week Ahead

Week Ahead

16 Jan 2026 12:52 GMT

WEEK AHEAD: China and Japan expected to hold rates amid Davos meeting

(Alliance News) – Interest rate decisions in China and Japan, plus inflation and unemployment figures in the UK lead the economic agenda, while the US earnings season picks up pace with results from Netflix, Intel and Procter & Gamble.

The following is a look ahead at the most important economic and corporate events globally in the days ahead.

Top economic events:

Monday 19 January

08:30 EST Canada CPI

10:00 CST China industrial production

10:00 CST China retail sales

10:00 CST China unemployment

10:00 CST China GDP

11:00 CET eurozone CPI

13:30 JST Japan industrial production

US Martin Luther King Jr Day holiday. Financial markets closed.

Tuesday 20 January

09:15 CST China interest rate decision

10:00 CET eurozone current account

08:00 CET Germany PPI

11:00 CET Italy current account

10:00 CET Spain trade balance

07:00 GMT UK unemployment

Wednesday 21 January

08:30 EST Canada PPI

10:00 SAST South Africa CPI

13:00 SAST South Africa retail sales

07:00 GMT UK CPI and PPI

10:00 EST US pending home sales

Thursday 22 January

11:30 AEDT Australia unemployment

16:00 CET eurozone consumer confidence

08:50 JST Japan trade balance

Japan BoJ meeting begins

07:00 GMT UK public sector net borrowing

08:30 EST US initial jobless claims

08:30 EST US GDP

08:30 EST US personal consumption expenditures

11:00 EST US Kansas City Fed manufacturing activity

Friday 23 January

09:00 AEDT Australia flash composite PMI

08:30 EST Canada retail sales

10:00 CET eurozone flash composite PMI

09:15 CET France flash composite PMI

09:30 CET Germany flash composite PMI

08:30 JST Japan CPI

09:30 JST Japan flash composite PMI

12:00 JST Japan interest rate decision

12:00 JST Japan BoJ quarterly outlook report

00:01 GMT UK consumer confidence

07:00 GMT UK retail sales

09:30 GMT UK flash composite PMI

09:45 EST US flash composite PMI

10:00 EST US Michigan consumer sentiment index

Top company events:

Tuesday 20 January

Alstom SA – Q3 results

Fastenal Co – full year results

Netflix Inc – full year results

Wednesday 21 January

Aberdeen Group PLC – trading statement

Burberry Group PLC – Q3 results

Currys PLC – trading statement

Experian PLC – trading statement

JD Sports Fashion PLC – trading statement

JD Wetherspoon PLC – trading statement

Rio Tinto PLC – trading statement

Travelers Cos Inc – full year results

Thursday 22 January

Intuitive Surgical Inc – full year results

Northern Trust Corp – full year results

Investor AB – full year results

Essity AB – full year results

Harbour Energy PLC – trading statement

Kimberly-Clark Corp – full year results

Procter & Gamble Co – half year results

Fortescue Ltd – trading statement

Alcoa Corp – full year results

McCormick & Co Inc – full year results

CSX Corp – full year results

Abbott Laboratories – full year results

Intel Corp – full year results

Friday 23 January

Ericcson AB – full year results

Here’s what to watch for as the week unfolds.

MONDAY to FRIDAY: The World Economic Forum could take on added significance this year amid increased geopolitical uncertainty, dominated by events in Ukraine, Iran, Greenland and Venezuela. The annual get together in the Swiss mountain resort of Davos brings together some of the most significant names in politics and business. According to the WEF website, 400 top political leaders – including close to 65 heads of state and government and six of the G7’s leaders – are expected to take part, plus nearly 850 of the world’s top business executives. US President Donald Trump will attend, as will Ukrainian President Volodymyr Zelensky, as talks continue aimed at ending the war with Russia. UK Chancellor Rachel Reeves will be there and is scheduled to hold a round table with business leaders hosted by JP Morgan boss Jamie Dimon. UK Prime Minister Keir Starmer’s attendance has not been confirmed. ECB President Christine Lagarde is speaking on two panels, although it is uncertain whether Federal Reserve Chair Jerome Powell will attend. Mark Carney, prime minister of Canada, Friedrich Merz, federal chancellor of Germany, and Ursula von der Leyen, president of the European Commission are among confirmed attendees.

MONDAY and TUESDAY: China is expected to leave interest rates on hold on Tuesday although the decision could be swayed by a raft of data the day before. Figures on economic growth, industrial production, retail sales and fixed asset investment are all due for release. Citi expects GDP growth at 4.6% year-on-year in the fourth quarter, which it notes is above 4.5% consensus but below the 4.8% growth reported in the three months to September. Industrial production could strengthen to 5.6% year-on-year in December from 4.8% in November, Citi thinks, reflecting the “beat” in PMI data. But retail sales are set to remain subdued, with Citi forecasting growth of 1.0% year-on-year in December, slowing from 1.3% in November, weighed by weak car sales. Fixed-asset investment could end 2025 with contraction of 2.8% year-on-year in December, Citi thinks, compared to a 2.6% on-year decline in November. Following the data dump, Citi expects the People’s Bank of China to leave the five-year loan prime rate unchanged at 3.5% and the one-year loan prime rate at 3.0%. Citi says the equity rally at the start of 2026 could make the central bank “more prudent” when it comes to cut. “A rate cut is still likely and plausible in our view in [the second quarter] but it may not happen in January,” Citi says.

TUESDAY: Jobs data in the UK is likely to confirm the employment market remained soft towards the back end of 2026, although some analysts see scope for the unemployment rate to nudge down from recent levels. Trading statements from recruiters PageGroup, Hays and Robert Walters all showed lower net fee income in the UK in the final three months of 2025, indicating less hiring, with PageGroup referencing “lower levels of confidence” in the UK. But brighter GDP data for November suggests some of the feared hit from the UK government budget may have been overstated. For the three months to November, RBC Capital Markets says that “with the fall in vacancies beginning to show signs of plateauing of late, we see scope for the unemployment rate to tick lower to 5%.” This would be down from 5.1% in the three months to October. RBC also thinks wage growth should continue to ease, with regular whole economy pay growth slowing to 4.5% in the three months to November from 4.6% in the three months to October. Private sector wage growth, which has slowed sharply in recent months, is seen cooling to 3.7% in the three months to November from 3.9% before.

TUESDAY: Netflix reports fourth-quarter earnings amid the backdrop of its USD82.7 billion bid for parts of Warner Bros Discovery. Los Gatos, California-based streaming service Netflix remains in pole position to secure the deal despite a competing offer from Paramount Skydance. Shares in Netflix have fallen 27% since the third quarter earnings print, with concerns about the deal and possible weak 2026 revenue guidance at the top of investor concerns. “The Warner Bros deal already raised organic growth concerns, and a soft FY26 guide would only intensify them,” says Jefferies in a research note. Jefferies says worries that guidance could come below the Street’s 13% year-on-year expectations has hurt confidence in the organic growth story amid heightened scrutiny given the Warner Bros bid. Jefferies’ analysts say hitting 13% revenue growth in 2026 requires ex‑ads average revenue per member to re-accelerate to 2.1% growth from 0.6% in 2025, which the investment bank calls “a tough ask”.

(continues)

Earnings Previews

Earnings Previews

04 Aug 2025 13:34 BST

EARNINGS PREVIEW: Diageo reports amid change at top and tariff worry

(Alliance News) – Diageo PLC is expected to report weaker annual results, in a set of annual results which will see tariff commentary and leadership transition in focus.

The brewer and distiller, which owns the Guinness stout brand and the Johnnie Walker whiskey range, reports annual results on Tuesday.

For the year ended June, Diageo is expected to report net sales of USD20.20 billion, down 0.3% from USD20.27 billion the year prior. Organic net sales growth of 1.4% is expected, according to company-compiled consensus.

An organic operating profit decline of 1.6% is expected. Reporting operating profit of USD5.65 billion is predicted, down 5.8% from USD6.00 billion.

In May, Diageo reaffirmed full-year guidance and said net sales in the three months to March 31 rose 2.9% year-on-year to USD4.38 billion from USD4.25 billion.

Diageo updated on tariff implications in that report.

“Assuming the current 10% tariff remains on both UK and European imports into the US, that Mexican and Canadian spirits imports into the US remain exempt under USMCA, and that there are no other changes to tariffs, the unmitigated impact of these tariffs is estimated to be USD150 million on an annualised basis,” Diageo said at the time.

But the tariff on Canadian imports is at 35%, and a US-EU deal meant a 15% tariff. Trump last week gave more time to neighbour and major trading partner Mexico, delaying for 90 days a threat to increase tariffs from 25% to 30%, after holding talks with President Claudia Sheinbaum. But it is also unclear what the tariffs mean for wine and spirits.

The EU said Thursday it expects its cherished wine sector to be hit along with most European products as US tariffs kick in this week, but negotiations were ongoing to secure a carve-out.

Brussels and Washington struck a trade deal at the weekend which will see most EU exports face a 15% US levy starting Friday, with a number of exemptions such as aircraft so far locked-in.

France, Italy and other wine making countries were pushing for zero tariffs for alcohol including champagne, wines and spirits among carve-outs in the final deal, but those talks were ongoing.

“It is not our expectation that wine and spirits will be included as an exemption in the first group announced by the US tomorrow, and therefore that sector, as with all other economic sectors, will be captured by the 15% ceiling,” European Commission spokesman Olof Gill told a press conference.

Diageo shares were down 0.9% at 1,806.50 pence each in London on Monday afternoon. The stock is down 23% over the past year.

“The company’s woes started with profit warnings in late 2023, with weakness in Latin America, along with a slowdown in the US prompted a sharp slowdown in sales. With concerns over tariffs adding additional headwinds, it’s not surprising that the shares have struggled, but have they fallen too far,” MCH Market Insights analyst Michael Hewson commented.

Hargreaves Lansdown analyst Aarin Chiekrie said Diageo’s third quarter performance was “rock solid”.

“Although these figures were flattered by customers stocking up on booze before the expected tariffs kicked in, there are early signs that the industry’s recovering from its cyclical hangover,” the analyst added.

“Markets will be keeping a close eye on just how well Diageo is managing these ongoing tariff headwinds, which were expected to add around USD150 million in annual costs. The Johnnie Walker and Guinness maker plans to absorb half through operational efficiencies, with the rest likely passed on through price increases.”

UBS believes Diageo’s organic revenue declined by 1.6% on-year in the fourth quarter, a better outcome than the 1.8% fall predicted by consensus, the Swiss bank said.

UBS sees a “negative impact from the reversal of trade loading ahead of tariffs in Q3”.

It added: “We are slightly more positive on Europe, with further upside risk in Africa and LAC, but downside risk in APAC.”

“Since our upgrade report to buy in December, our US recovery thesis has not played out as expected. However, following the recent de-rating and current depressed valuation multiple, we think the stock can work over the next 12 months as we expect improving earnings and cashflow visibility from accelerating self-help measures,” UBS said. “We see upside risks building to FY26 earnings from margins and FX.”

Tariff worries have hit Diageo shares, but AJ Bell analysts believe other factors are also at play.

“The shares, and expectations, have been weighed down by fears over the impact of tariffs, a change in drinking habits, especially among younger generations who seem to consume less alcohol, and also trading down, as inflation and a soft economic outlook persuade drinkers to switch to cheaper brands. It may also be that Diageo is now paying the price for its prior ‘premiumisation’ strategy and witnessing a return to more normal drinking patterns as lockdowns fade into the memory and more workers return to the office,” the AJ Bell analysts said.

Diageo is on the hunt for a new boss after Chief Executive Debra Crew stepped down in July by mutual agreement. Chief Financial Officer Nik Jhangiani has taken the helm in the interim, while former finance chief Deirdre Mahlan temporarily becomes CFO.

Crew’s tenure was marked by a profit warning, scrapped growth targets, and a sharp decline in the company’s share price. Crew had led Diageo since June 2023, having joined as a non-executive director in 2019 before taking on the role of president of Diageo North America and chief operating officer.

Chiekrie commented: “Former CEO, Debra Crew, stepped down with immediate effect in mid-July, after more than two years of relatively underwhelming group performance, so investors are keen to get some updates on the search for a longer-term successor.”

Jefferies believes Jhangiani can bring “fresh perspectives” on cost discipline, deleveraging and “sharpening execution to drive greater consistency of delivery”.

“This will underpin USD3 billion of free cash flow in [financial 2026] as well as operating leverage,” the broker added.

By Eric Cunha, Alliance News news editor

Comments and questions to newsroom@alliancenews.com

Copyright 2025 Alliance News Ltd. All Rights Reserved.

Central Bank Previews

Central Bank Previews

18 Dec 2025 03:03 GMT

BOJ PREVIEW: Analysts expect rate hike and signal further rises

(Alliance News) – The Bank of Japan is widely expected to raise interest rates by a quarter point this week to its highest level in three decades, as policymakers contend with persistent inflationary pressures and a weakening yen.

Japan’s central bank last revised its short-term policy rate in January with a 25 basis points hike to 0.5%, the highest in 17 years. Policymakers have held the rate steady at subsequent meetings in March, May, June, July, September and October.

In October, the decision was split seven to two, with board members Naoki Tamura and Hajime Takata proposing a 25 basis point hike.

The BoJ will announce its rate decision at midday in Tokyo, 0300 GMT, on Friday.

In a Reuters poll, 90% of economists, or 63 of 70, expected the Japanese central bank to raise short-term interest rates to 0.75% from 0.50% at the December meeting.

Last month’s data from the Statistics Bureau of Japan showed that consumer inflation edged higher in October, with headline and core CPI both rising to 3.0% from 2.9% in September. It is above the BoJ inflation target of 2%.

Kathleen Brooks, research director at XTB, said: “This is likely to be enough evidence for the BoJ to embark on a much-anticipated hike, there is currently a 92% chance of a hike priced into the interest rate swaps market, which suggests that the financial markets are marginally more convinced about a BoJ hike this week… We expect them to take a cautious tone and to refuse to signal when or if future hikes are coming.”

Analysts note that market conviction has firmed in recent weeks, with expectations shifting decisively toward a December hike.

RaboResearch Senior FX Strategist Jane Foley commented: “The market now strongly expects a 25 basis points hike. This marks a sharp shift in sentiment since, as recently as October, Sanae Takaichi’s appointment as PM had sparked widespread fears that she would lean on the central bank not to tighten policy.”

Min Joo Kang, ING senior economist for South Korea and Japan, also believes that a hike is imminent, noting robust export growth for a third straight month that swung Japan’s trade balance to a JPY322.23 billion surplus in November from a JPY231.77 billion deficit in October.

“We don’t expect Governor Kazuo Ueda to send any hawkish-tilted messages to the market at the presser, given growing concerns about rising market rates. The BoJ expects real rates to remain negative after the rate hike later this week, leaving room for further hikes,” Kang said.

Wells Fargo economist Brendan McKenna had also been steadfast in their view of a rate hike, commenting: “Our rationale for a hike came down to our assessment of underlying economic fundamentals in Japan which—despite political preference for easier monetary policy after Prime Minister Takaichi’s election earlier this year—we felt were consistent with tighter BoJ monetary policy. This conviction stems from wage hikes that are above the current pace of inflation, fiscal stimulus deployed by the Takaichi administration and leading indicators that suggest activity is still firm.”

Furthermore, Kelvin Lam an analyst at Pantheon Macroeconomics, said: “The BoJ has previously cited lingering trade uncertainty as a key reason for pausing policy normalisation, and now that risks have been greatly reduced—with even China managing to forge a temporary trade truce with the US at least until November 2026, effectively eliminating the economic risks induced by third-party trade actions—conditions appear more supportive.”

Goldman Sachs noted that at the BoJ’s last meeting, Governor Ueda signalled the timing for a rate hike is drawing closer, citing developments in the US economy and confirmation of wage momentum in next year’s shunto spring negotiations as key conditions.

“While Governor Ueda’s speech did not explicitly signal a December rate hike, it paves the way for a December hike if wage increase momentum can be confirmed,” Goldman said.

Pantheon Macroeconomics believes that the BoJ’s recent research, showing 29 out of 33 branch offices expect wage growth to remain broadly unchanged next financial year, underscores how labour shortages rather than profitability are driving pay hikes.

“Moreover, the BoJ concedes that pay growth is likely to fall behind at small businesses, which lack pricing power, and auto manufacturers, whose margins have been slammed by US tariffs, even after the US-Japan trade agreement.

“We think this report offers enough fuel for the BoJ to justify a 25 basis points policy rate hike to 0.75% on Friday, especially given the recent currency weakness and sustained food inflation,” it said.

Sumi Trust economists commented that the BoJ faces a more favourable backdrop for tightening policy.

“We anticipate attention to centre on whether the BoJ proceeds with additional rate hikes. Persistently high inflation, clarity emerging on US-Japan tariff negotiations, and ongoing corporate wage increases have created a more favourable environment for tightening monetary policy. However, with the inauguration of the Takaichi administration, seen as supportive of continued monetary easing, some market participants believe the BoJ will take a more measured approach on rate hikes,” Sumi Trust economists said.

Citi analysts highlight the BoJ’s policy signals, noting: “We believe a key focus point is the extent to which the BoJ signals future rate hikes amid a weak yen trend. However, rather than this shifting the yen to a strengthening trend (which looks fairly unlikely), we believe the BoJ may be satisfied if the yen does not depreciate further.

“If yen depreciation accelerates in January-March there is a risk the rate hike could be brought forward. The market’s terminal rate pricing is in the mid-1% range, and 10-year bonds should see solid demand in the 2% range. Investors may further avoid duration exposure if the size of fiscal measures increases.”

The dollar was buying JPY155.79 around 0300 GMT on Thursday.

Bank of America also expects a hike to 0.75% this week, followed by further increases every six months in June 2026, January and July 2027, predicting it will reach 1.5% by the end of 2027.

“We think the MPM statement will maintain the BoJ’s baseline scenario for current economic conditions and the outlook, which states that tariffs will result in slowing growth in overseas economies, but we expect it to acknowledge that downside risks and uncertainties regarding its outlook have diminished…While the BoJ might send some message about the neutral rate of interest (and terminal rate) at the post-MPM press conference, we think it will struggle to give the kind of explicit guidance about the level of the terminal rate that the market wants.,” BofA said.

UBS economists share the sentiment, citing “favorable economic growth and progress in underlying inflation” as paving the way for a semiannual pace of rate increases to 1.25% by end of 2026 and a terminal rate of 1.5% by mid‑2027.

ING’s Kang weighed in on future hikes and commented, “Current market expectations point to an additional rate hike in June or July. However, our assessment indicates that October is more likely. We anticipate that BoJ will maintain its existing neutral rate estimate within the 1-2.5% range for the foreseeable future.”

With conviction firm and inflation pressures persisting, markets await the BoJ’s announcement on Friday for clues on whether further tightening lies ahead.

By Judy Amaca, Alliance News reporter Asia-Pacific

Comments and questions to newsroom@alliancenews.com

Copyright 2025 Alliance News Ltd. All Rights Reserved.

Global Calendars

Global Calendars

20 Jan 2026 12:44 GMT

Global company events calendar – next 7 days

| Wednesday 21 January | |

| Aberdeen Group PLC | trading statement |

| Burberry Group PLC | Q3 results |

| Currys PLC | trading statement |

| Elementis PLC | trading statement |

| Experian PLC | trading statement |

| Hochschild Mining PLC | trading statement |

| ICG PLC | trading statement |

| JD Sports Fashion PLC | trading statement |

| JD Wetherspoon PLC | trading statement |

| Johnson & Johnson | full year results |

| Premier Foods PLC | trading statement |

| Quilter PLC | trading statement |

| Rio Tinto PLC | trading statement |

| Snam Spa | dividend payment date |

| South32 Ltd | trading statement |

| Travelers Cos Inc | full year results |

| Thursday 22 January | |

| Abbott Laboratories | full year results |

| AJ Bell PLC | trading statement |

| Associated British Foods PLC | trading statement |

| Auction Technology Group PLC | AGM |

| CSX Corp | full year results |

| Fortescue Ltd | trading statement |

| Harbour Energy PLC | trading statement |

| Intel Corp | full year results |

| Intuit Inc | AGM |

| Intuitive Surgical Inc | full year results |

| Procter & Gamble Co | half year results |

| Santos Ltd | full year results |

| Sirius Real Estate Ltd | dividend payment date |

| Friday 23 January | |

| Cranswick PLC | dividend payment date |

| SSP Group PLC | AGM |

| Monday 26 January | |

| Baker Hughes Co | full year results |

| Tuesday 27 January | |

| Alexandria Real Estate Equities Inc | full year results |

| American Airlines Group Inc | full year results |

| Boeing Co | full year results |

| Cranswick PLC | trading statement |

| Dr Martens PLC | trading statement |

| Mitie Group PLC | Q3 results |

| Roper Technologies Inc | full year results |

| Sage Group PLC | trading statement |

| Texas Instruments Inc | full year results |

| Union Pacific Corp | full year results |

| Visa Inc | AGM |

| WAG Payment Solutions PLC | trading statement |

| Comments and questions to newsroom@alliancenews.com | |

| Copyright 2026 Alliance News Ltd. All Rights Reserved. |

Top News

Top News

Service Comparison

AWP Alliance News

Global Professional

Alliance News

Global 500 Professional

AI summaries - 20,000

Companies - editorial coverage

Markets

Economics